“We have, in this country, one of the most corrupt institutions the world has ever known. I refer to the Federal Reserve Board. This evil institution has impoverished the people of the United States and has practically bankrupted our government. It has done this through the corrupt practices of the moneyed vultures who control it.” – Congressman Louis T. McFadden in 1932 (Rep. Pa)

They finally told the truth about who really owns the currency, though not in plain English. They do not explain their actions nor their comments on the economy in plain English. One has to deduce and discover the proper purpose and meaning. Here is how you know that there is something seriously wrong with your understanding of the USD and the federal reserve: the 2010 Wall Street Reform and Consumer Protection Act (the Dodd-Frank Act). This bill is insidious! Before the bill, when you put your currency in the bank or purchased a bank CD, you become a debtor and the bank became the creditor. They owed you your deposited currency on demand or the value of your CD either when terminated or expired. Now, when you place your currency in the bank, you become an unsecured creditor and the bank is the debtor! You just loaned what you thought was your currency to the bank! Furthermore, you are last in line to get your money if the bank fails! Thus, you assume the role of an unsecured creditor.

No way? Read about the plan: Dodd-Frank Kills: How The U.S. Joined The International Bail-In Regime

And we are lead to believe that the FDIC is there as a backup to make us whole should the bank be unable to pay their debt to you. You can read about it here: Resolving Globally Active, Systemically Important

Do you understand what this means? When you deposit your currency into your bank account, you are loaning your currency to that bank. It is no longer your currency. It never was anyway nor will it ever be yours. It has turned into a loan. Like any loan, the debtor– the bank– can only pay back the creditor– you– if they have the currency to pay. Instead, they have written into the law that the bank can repay in shares of that bank if there is a bank failure. Great! You receive shares of a bankrupt, worthless bank. The strange paper bets called derivatives, aka risky bets made by the banks, are even paid first. Great. There are TRILLIONS of $$$ in derivatives. You are an “unsecured” debtor! You have no leverage or claim.

How can bankers do this? How is it that the politicians sponsored, wrote, and passed this law? They understand something that you do not. You do not own that dollar. You are simply being allowed to use it. That is why they can take it from you, inflate it, outlaw it to go cashless, tax it, hypothecate it (add your deposit with many others and then use the total sum as collateral), pay you negative interest (which is a technical default, since you are owed at least what you deposited), and of course simply seize it using the IRS or the revenuers– civil asset forfeiture– if you are pulled over. It’s similar to a banker coming to your house and driving the car that you thought you owned. So where does this leave you and I? I am feeling the noose!

Why did I not go the way of my friend, Vern? I knew how to live separate of this currency system 35 years ago! He built a number of homes, sold them, and turned all of the profits into gold and silver. He kept a piece of land and built a tiny home for himself, living off of the grid. He does odd jobs from time to time for cash. He has established an open case in District Court establishing himself as a private citizen, not a sovereign citizen. Sovereigns are kings and queens and bunk. He declares that he is not a corporation and rejects being under the corporate umbrella of the United States of America Incorporated. Read about the Act of 1871. How do you like being ruled by a heartless, deceiving, sleazy corporation?

His open case clearly instructs all parties part of or affiliated with USA, Incorporated that they are to address him as a private citizen further stating that they do not have legal authority over him. Of course, he is correct. It’s kind of the same principle as a county sheriff. Thus, he has alleviated himself from the responsibilities that emanate from the contract with USA, Inc. and their USD. Everything you sign, all of your legal documents that identify you, and all of your contracts are in capital letters– the hallmark of a corporation. It all started when you were signed up for a Social Security card. I pondered keeping my children from the contract with USA, Inc. However, I did not want to set their future. Living like Vern allows you to drive the highways without a license, hunt and fish without a license, and barter without paying taxes. However, he does pay property tax as the tribute to the king! The only problem is that authorities will stop you and harass you every time they happen upon you outside of your home. They do not understand the fairly complex web of common law that gives one personal rights that trump the state’s assumed, aggressive authority. Once they review the federal case, they let him go. That lifestyle has a high PITA factor.

He is somewhat of a fraud, or perhaps I am too much the purist, in that he trades a gold piece for USD from time to time to commence commerce in USD. I say if you need to live separate from the corporation, setup your bartering chain, trading goods and services much like the eras before the Federal Reserve System began. If he desires to perform a transaction that requires an ID, he has to employ proxy corporate citizens to transact for him within the USD/USA Inc. world.

Like I said, I knew of the private citizen lifestyle years ago. Living like Vern does not attract the babes. Imagine your car is towed on a date with a lady because you have no plate! Instead, you have a legal document of a private citizen. The dude that pulled you over will most likely think there is something wrong with you! Instead I exposed myself to our debt-based system in return for a lifestyle of relative ease. The only problem was that I knew I had to make choices that would guard me, as much as possible, from the banking thieves and their government and media accomplices. Vern is fully protected. Once you understand this place where you live, life requires decisions that the normal Joe would think are insane. For example, I have a 401k, savings, a TDAmerica account, and trade options, bank accounts, credit cards, a small corporation, and a job. I pay taxes, sell on eBay, and sell on several websites. I hide in plain sight. To the thief– any government entity– I appear normal. However, what they do not know and what most people cannot comprehend is that I decided to become my own central bank. I am one of the “one in a million” that understands this devilish scheme.

I had decided to split earned currency into three structures– 401k, land, and gold/silver. I surmised that when they pay SSN at the time of declared eligibility, the purchasing power would be dismal, near worthless. However, they would have fulfilled their legal obligation to pay that monthly stipend. There are some natural laws that cannot be violated. They know that very well. Why would I state that I expect to be paid in a near worthless monthly stipend? Take a look at this:

It is obvious my purchasing power is plummeting. We’ve been hit with higher prices, same price lower quantities, and in some cases lower quality same price. I sense that I am being taken as a chump when I hear the government tell me that inflation is 1%-2% per year. They know quite well that the inflation rate, as calculated after the 1980s, does not reflect everyday life.

Of course, there are always the delusional amongst us. In response to the above graph, I saw the following post on Pragmatic Capitalism, Practical Views on Money, Finance & Life:

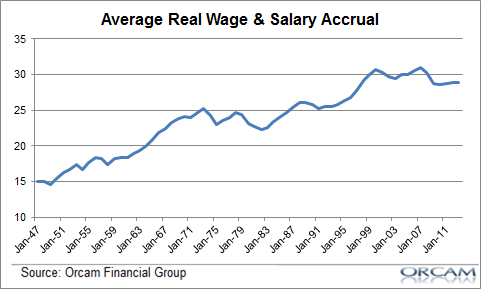

“I recently saw a web post comparing the salary accruals on a per capita basis.” (He is referring to the graph below. Accruals are nothing more that accumulated wages not yet paid. It’s like getting a pay check every two weeks. The amount is accrued or added up until paid.)

(WOW! That looks pretty good! Wages and salaries on an upward trend.) Continuing with the comment:

“So, it’s important to put this, the Purchasing Power of the USD chart above, in the right perspective here. And when we look at this discussion it’s best to use an inflation adjusted perspective of wages and salary accruals on a per capita basis. And when we run that figure the chart looks a lot different and you’ll notice that our wages today buy twice as many goods and services than those wages could afford in 1947. (the chart only went back to 1947)”

Okay, I guess that clears it up! He is saying that the purchasing power graph above is nothing more than a symptom that when weighed with the wages and salary accrual increase makes that balance even. Really? I could say let’s examine our personal life to determine what is really true. Do these equal? Can you purchase the same amount of goods when compared to 10 years ago? I know that I cannot! Refer to the coffee example above! He fails to include, or subtract, real inflation impact to that rising but inflation affected wage. Let me find an article from one of the accomplices to see if the accrual comment stands. This should be easy.

From CNBS.com

A Long, Steep Drop for Americans’ Standard of Livingby Ron Scherer of the Christian Science Monitor, Wednesday, 19 Oct 2011:

“Think life is not as good as it used to be, at least in terms of your wallet? You’d be right about that. The standard of living for Americans has fallen longer and more steeply over the past three years than at any time since the US government began recording it five decades ago.

Bottom line: The average individual now has $1,315 less in disposable income than he or she did three years ago at the onset of the Great Recession – even though the recession ended, technically speaking, in mid-2009. That means less money to spend at the spa or the movies, less for vacations, new carpeting for the house, or dinner at a restaurant.”

Or better yet: Invisible American

“The percentage of Americans who say they are in the middle or upper-middle class has fallen 10 percentage points, from a 61% average between 2000 and 2008 to 51% today.”

Do you understand? I could go into the unemployment figures to further prove my point that we are living with a giant blood sucking bed bug that only comes out to feast for its life’s blood, currency, and control to spread more lies that justify their thievery. How truly sad for the poor and those on a fixed income! That is why I have always considered the color of currency to be red, not green! As a matter of fact, this is so egregious that I have to show you.

paulcraigroberts.org: Employment Lies — Paul Craig Roberts, June 3, 2016

“June 3, 2016. Today the Bureau of Labor Statistics announced that the US economy only created 38,000 new jobs in May and revised down by 59,000 jobs the previously reported gains in March and April.

Yet the BLS reported that the unemployment rate fell from 5.0 to 4.7 percent, a figure generally regarded as full employment.

The May jobs increase only covers a small fraction of the monthly growth in the labor force and, therefore, cannot account for the drop in unemployment.

Moreover, the BLS reported that the labor force participation rate fell by 0.2 percentage points, bringing the decline to 0.4 percentage points over the past two months. Normally, a strong labor market, such as one represented by a 4.7% unemployment rate, causes an increase in the labor force participation rate.

The question becomes: How real is the 4.7% rate of unemployment?

The answer is: Not at all.

The unemployment rate dropped because people unable to find jobs ceased looking and are no longer counted as being in the labor force. If you are unemployed but not considered part of the labor force, you are not included when unemployment is measured. The BLS says that in May there were 1.7 million Americans who “wanted and were available for work,” but “were not counted as unemployed because they had not searched for work in the 4 weeks preceding the survey.”

In other words, the unemployment rate is a useless measure of unemployment, just as the consumer price index no longer measures inflation. What were once useful statistical measures have been converted into good news propaganda.”

And more dissecting the unemployment lie:

- Fortune: Is the unemployment rate really just a “Big Lie”? by Chris Matthews, February 4, 2015, 7:00 AM EDT

- thebalance.com: What Is the Real Unemployment Rate? Does the Government Lie About Unemployment? Kimberly Amadeo, Updated September 02, 2016

Wait, there is more of the lie! Recently I saw the headline that there has been a 5% increase in median household income. That kind of gives you good, hopeful feelings. It brings an easing of the mind. It’s reassuring that the economy is “on the right track”. I knew immediately that was a misleading statement meant to give the illusion that incomes are rising. They assume that you, yes you and I, have no idea what a median amount really means. Here is a good explanation.

An excellent graph that shows the same taken from the oftwominds article above:

Here is the real picture. “The truth is the rich are getting richer and everyone else is losing ground as inflation chews through stagnant incomes.”

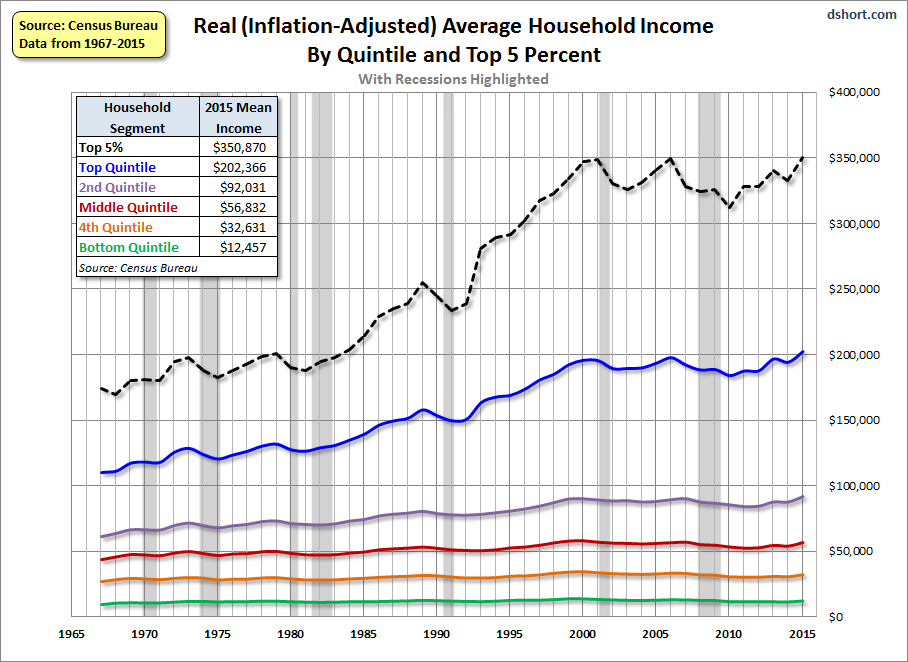

As we hear ad nauseam that rich are getting richer, the poor are getting poorer. Let’s take a look at the real data after being adjusted for inflation. That is government calculated inflation not the real numbers from before the 1980s as discussed previous. Who really grew 5% in 2015? The following chart breaks the household income into two distinct groups– ones at or above $200,000 and those below. There is a simple example of median at the end of this document.

IT’s nothing but a deceptive lie! Did you review the remaining two graphs in the oftwominds article?

- Increases in household wealth continue to accrue to the top of the wealth pyramid: The “Devastating” Truth Behind America’s Record Household Net Worth.

- If CPI is used, the “real median household income” has not even regained its 2008 level.

Got it? Just in case you have doubt, let’s review. From the oftwominds article:

If “real” inflation is running hotter than “official” inflation, which it is if we properly weight the big-ticket items such as rent, healthcare, and college tuition, then “real household income” has declined sharply since 2008; the 5% “gain” is completely illusory.

http://www.oftwominds.com/blogaug16/burrito-index8-16.html

http://www.oftwominds.com/blogaug16/inflation8-16.html

http://www.oftwominds.com/blogaug16/inflation-crash8-16.html

NOTE: From 1913 until now, inflation of the dollar has been 2950%. A 1913 dollar would now be worth $.034. When I became a wage earner in 1950, I could buy a full breakfast, eggs, sausage, hashbrowns, shortstack, juice, and coffee for $0.39. This morning I paid $9.60 for the same; that is an inflation of 2460%!

And one more as observed at zerohdge.com:

The Dying Middle-Class, by Tyler Durden – Sep 27, 2016 8:00 PM

Authored by Bonner & Partner’s Bill Bonner (annotated by Acting-Man’s Pater Tenebrarum),