The financial services industry is headed for the greatest debate in recent history.

Regardless of what occurs from here –a continued stock market bullish trend or reversion to long-term averages which chronicles back to 2000 levels, the confines of discussion, the heated verbal and written volleys tossed deep from the roots of philosophical differences will forge a permanent rift between the steadfast buy-and-hold brethren and the stewards who manage risk by preserving capital (the dreaded group with a market escape plan), through the forthcoming bear cycle.

The stakes are higher than I can recall.

Future generations: Those we are depending on to lift the globe from the depths of a demographic malaise, groups nowhere near as ostentatious as Baby Boomers; generations that savor experience over product and have been wary of the risk in stocks, are beginning to relent and take notice of this bull market trajectory.

How they experience the ride in stocks and what occurs from here will shape their investment philosophy. I fear Millennials to Gen Y are going to get fooled, taken out. Smacked in the face.

Betrayed.

The buy-and-hold side, ‘the setters and forgetters,’ which I’ll explain, appear to be winning this battle so far and that’s part of the reason for my concern and ironically, a matter-of-fact bullishness.

For now and the near future it’ll be hunky dory. You see, I think we are in the midst of witnessing the greatest market bull stampede since 1995 through 1999. I believe it’ll eventually make the tech bubble explosion sound and feel like a 5-year old throwing down in joy, a bang pop noise maker on hot cement through a humid-heavy July 4th.

However, this is just my humble opinion.

I hold the utmost respect for the market as it’s designed to fool me as much as possible and at every gyration. I’m open-minded and with the assistance of our no-spin, in-house data crunching at Real Investment Advice, I remain more eagle, or eye witness, as opposed to a ‘bull’ or ‘bear.’ And I observe here, the beginning of the “bubble’s bubble.”

The break out of a long-term sideways market cycle which began in 2013, stalled in early January 2015 when the S&P 500 closed at 2058. On November 9, 2016, it stood at 2163. Watching paint dry through the summer of ’16 would have been more exciting than the market action. It was torturous. I described it to Lance Roberts at the time as suspended animation.

Then the presidential election happened and the rest is history…

I’m hesitant to refer to the current market as a bubble. I refer to it as the boom that leads to a bubble. See, my definition, perception, differs from market soothsayers. It isn’t in a textbook. It emerges from my boyhood summer activities on a New York street. The greatest bubbles I recall were the largest ones, most magnificent, right before they burst in a soapy, rainbow mess, stung my eyes like slimy razors, and forced me to lament through a wince:

“Wow – that was freakin’ incredible!”

The current Shiller Price-Earnings Ratio stands at 29X; the tech-wreck Shiller was a hair short of 45X in December 1999. My definition of bubble begins at the apex of the ‘pop’ of the previous high. From there, I believe only if or when we exceed that limit, that the market should be deemed the “bubble’s bubble.”

For now, I’m going to outline the factors or input that is breathing sustainability into this phenomenon.

Don’t misunderstand: My belief is when this market adjusts, there’s going to be stinging eyes from tears spilled over brokerage statements and the mutter of “I got suckered again,” over and over.

You see, every bubble differs in composition. The boom-bust cycle feedback loop we’re traveling now isn’t fueled by an industry or sector. It’s greater in scope. The wind in the proverbial sails is a confluence of factors fueled by post-election animal spirits and a lower-than-longer interest rate environment which is the prime food source or hive for the bull.

Poor demographics, below-average productivity which keeps the Federal Reserve and yield curve captive in a flat wasteland of inertia, a new generation of financial professionals who never experienced a bear market, an overwhelming number of passive preachers who believe indexing (without regard to risk management), is some form of financial nirvana, a brokerage industry under pressure to comply with a looming Department of Labor fiduciary standard slated implementation on June 9, stirred with the hope of corporate tax reform ‘sometime in the future, (it’ll be big)’, boils a seductive porridge the bubble’s bubble can’t get enough of.

Regardless of the possible repeal or modification of the DOL ruling under the current presidential administration, investors are demanding a greater standard of care from those who assist them.

Big box financial retailers are desperately scrambling to create procedures designed to reduce possible liabilities that come from taking on fiduciary responsibilities. The last thing on their minds is to “do what’s in the highest best care of the client.” The paramount concern is to work with their cadre of lawyers to minimize business risk for themselves. The investment risk you absorb will remain of little concern except for how thinly they determine your ‘risk profile.’ As long as your responses to risk queries are recorded, you’re screwed.

A method I know is growing popular with several financial behemoths is to take the portfolio decisions out of the hands of otherwise knowledgeable employees and place them with a group in a centralized location thus creating a homogenized, factory assembly-line process allegedly for closer monitoring.

Strangely, and perhaps insidiously, I wholeheartedly believe the intention is to build closer ties to the firm thus severing the relationship with the adviser, who is always deemed a flight risk. This method also frees up frontline professionals to sell more packaged asset-allocation product or you got it, feed the profit-margin beast.

The next bubble pop may be a game changer for the industry again and motivate financial professionals who do a magnificent job of selling products or outsourcing money management which ostensibly distances themselves from ground zero of an imminent explosion (hey, it’s the market, not me), to possibly re-think their careers. Take on a fiduciary calling.

Perhaps a bubble or at the least, a severe bear market is required to cleanse the system, drain the swamp, by migrating miscreants to more fitting livelihoods like pushing phone service deals at T-Mobile or taking roles as activities directors for Carnival Cruise Lines. We’re due.

It’s a romantic notion. A nice thought. Meh, it keeps me motivated to consistently provide what I consider ‘full circle’ financial guidance, the complete story, pros & cons, and planning for risk markets that we strive for at Real Investment Advice.

While we await comeuppance, let’s review what stirs inside the bubble’s bubble.

The ‘passive’ revolution we’re witnessing is to provide a portfolio solution which is based on the demand for the products, regardless of how expensive the products may be.

To be clear, I’m an advocate for index investments and lower internal portfolio costs. I was one of the first financial professionals at my former employer to use market cap weighted exchange-traded funds in client portfolios to replace mutual funds.

My beef is how indexing is perceived by unsuspecting investors as safe and insidiously branded or allowed to be positioned by the buy-and-hold faction, as the ultimate never-sell strategy.

Not because it’s best for the investor; well, that’s a convenient half-truth. Mostly, it’s optimum for the adviser under pressure who can offer a pretty asset allocation solution in a package and move on to the next notch on the sales belt.

The front-line consultant of a publicly-traded big box financial retailer is under never-ending intense pressure to increase margins for shareholders. The performance of the stock price is the priority. I was provided this wisdom, which I have never forgotten, from a former regional manager at Charles Schwab – “It’s shareholders first; then follows the rest of us, including clients.”

If passive is what clients want, passive is what they shall receive, but in a manner that can be delivered and scalable by a financial retailer in a CYA/fiduciary manner. It’s time efficient to get cash fully invested in an asset allocation at once; buy full in to the story that it’s time in the market not timing the market, regardless of current valuations or expected returns, especially as corrections appear more as distant memory than reality. READ: The Deck is Stacked: Putting Risk and Reward into Perspective.

Here’s how I see it as the bull rages on:

The asset allocator factory box designers are diligent at work, creating neat, easy-breezy investment packages positioned as products or “solutions,” thus forging a path perhaps we haven’t walked so passionately before.

The demand for these attractive boxes filled with a colorful palate of panacea in the form of passive investments, may drive valuations higher than we’ve seen, even greater than the tech bubble, which will leave investment veterans perplexed.

Market this sausage to a new breed of adviser who perceives passive as safe, has rarely witnessed a correction or bear market working in the trenches with clients, and serve it up on the finest wrapper Wall Street marketing has to offer, and God help us.

Why?

The investment vs. valuation connection is aggressively being severed. Asset-allocation solutions are being positioned to ‘pros’ as simple, third-party adjuncts to an overall financial planning experience. The intoxicating promise of ease and low cost which places what you pay in the form of valuations in a clean-up spot, or makes it an afterthought (if that), is incredibly alluring. Buy it up now, let it grow, harvest later. Simple.

After all, stock valuations are as easy to comprehend as nebulae millions of light years away.

So why bother?

Just buy the box. Open in 20 years. Hopefully, just hopefully, there’s something in there to show for it.

The demand for the product of stocks to market and maintain aggregate static asset allocation programs overrides the price paid for that product.

One of the best blogs I’ve read about “earningless” bull markets and the overall demand for stocks comes from www.philosophicaleconomics.com in a piece penned The Single Greatest Predictor of Future Stock Market Returns.

At this juncture, a lack of viable alternatives, the massive growth of robotic allocations of passive investments packaged and sold, and the aversion of the corporate sector to issue new equity has created a demand for stocks similar to the demand for a product, like an IPhone. Regardless of price, if the IPhone is in demand, you’ll stand on line for days to get it. It doesn’t need to make sense, don’t try to rationalize it.

From the blog post:

Ultimately, the price of equity is determined in the same way that the price of everything is determined–via the forces of supply and demand. For any given stock (or for the space of stocks in aggregate), price is always and everywhere produced by the coming together of those that don’t own the stock and want to allocate their wealth into it, and those that do own the stock and want to allocate their wealth out of it.

It’s all up to the allocators–they decide how much of their wealth they are going to allocate into stocks, how much exposure they are going to take on. Their preferences–or rather, their efforts to put those preferences in place, by buying and selling–set the price. Valuation is a byproduct of this process, not a rule that it has to follow.

Buy-and-hold is painted as the informed, responsible, pro-American thing to do with a portfolio. But, in terms of financial stability, it can actually be a very destructive behavior. Consider the classic buy-and-hold allocation recommendation: 60% to stocks, 40% to bonds (or cash). What rule says that there has to be a sufficient supply of equity, at a “fair” or “reasonable” valuation, for everyone to be able to allocate their portfolios in this ratio? There is no rule.

If everyone were to jump on the buy-and-hold bandwagon, and decide to allocate 60/40, but equities were not already 60% of total financial assets, then they would necessarily become 60% of total financial assets. The excess bidding would not stop until they reached that level. It doesn’t matter that the associated price increase would cause the P/E ratio to rise to an obscenely high value. The supply-demand dynamic would force it to go there.

If aggregate demand for stocks continues, then valuations will be an afterthought. However, there is a risk to this rosy scenario. Currently, household equity percentages among individual investors stand at their highest level in two years at 67.6% per the March AAII Asset Allocation Survey. Prior bull cycles have seen equity allocations exceed 70%. Granted. Yet, consumer sentiment or the ‘feel good factor’ is at thresholds we haven’t crossed since 2004. Confusing.

Keep in mind, stocks don’t need to correct exclusively in price, they can in time. In other words, the higher valuations our team calculates for stocks can even out over the next few years ostensibly pulling down the long-term averages of stocks to 2%, maybe less.

And the reward for stock risk flies in the face of Warren Buffett’s commentary that “bonds are lousy investments.” Let’s see – 2% with 100% probability of recovering my principal at the end of a period or 2% return with a tremendous chance of loss at the roulette wheel. Hmm…

The demand for risk assets is going to require several conditions to remain consistent. I’ll cover what I consider the most important.

Which gets me to:

Passive investing is exploding in popularity. I’m concerned about the true reasons why.

From a recent article in the L.A. Times:

When money flows into conventional index funds, they must buy the stocks in their index regardless of the underlying companies’ financial health or outlook.

“Of course it distorts things,” said Rob Arnott, who has pioneered a fundamentals-based form of indexing at Research Affiliates in Newport Beach. “Price discovery,” the term for research that gets to the heart of a stock’s relative value, “is diminished as fewer and fewer investors care about the fundamentals,” Arnott said.

The migration to passive investments is indeed exploding. Currently, 42% of all U.S. stock funds are in passive vehicles.

One reason is indeed lower costs. Indexing is definitely a bargain TYPE of investment (more on this coming), when compared to many actively-managed funds. Low internal fees is a positive for investors.

Unfortunately, I believe the overwhelming reason for the massive popularity of passive investments is performance or outperformance when compared to their actively-managed colleagues; the market momentum we’ve been experiencing since 2009 fueled by strong tailwinds of prolonged low rates, multiple quantitative easing programs, corporate share buybacks, and companies that operate lean and mean (it’s always a recession in corporate America when it comes to employee headcount), have forged accelerants to market increases.

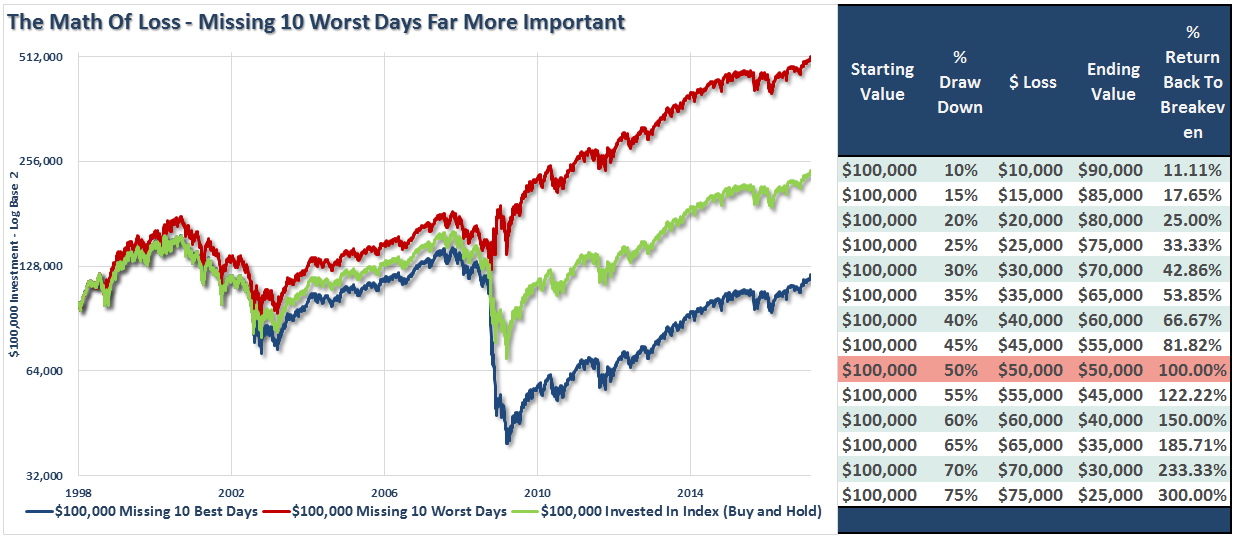

However, cycles do change. Yet, nothing about that fact from passive preachers. Zero about bearing the full brunt of stock market risk. Nada about the math of loss.

Which gets me to:

Passive investing is not safe. Not by a long shot. To clarify: Passive is an investment type. It is NOT an investing process nor a manner to which RISK is managed.

The clearest thought I can conjure up about passive investments and bear markets is I have the finest potential to lose money at low internal costs. Never forget – Once wealth is allocated to stocks, it’s active. On occasion, radioactive. Plain and simple. Index positions must be risk managed. They bear the full risk of markets. The highs and the lows. There’s no escape-risk-free card for you.

The passive preachers make it sound like once you’re indexing there’s no need to manage risk. Diversification is supposedly the only means to do so, but beware. How you define diversification differs from how your broker does. READ: Never Look at Diversification the Same Way Again.

The granddaddy of indexing Jack Bogle of Vanguard readily tells the media that stocks are ‘overpriced.’ Future returns will be below average. In the next breath, he’ll suggest go all in because there’s nothing else you can do. If anything, that’s a pretty dangerous passive attitude to have considering the wealth carnage from math of loss, which again, is a topic that is never discussed.

Go for it. Select your own index or exchange-traded funds or work with a fiduciary to create an asset allocation plan. Regardless, a rules-based approach to rebalance overheated asset classes or exit stocks surgically through market derails as identified in Lance Roberts’ weekly newsletter, should be part of the process. That’s a full-circle approach to investing – The buy, the hold and the other four-letter word – Sell.

I’d keep the “sell” word on the “down low” with your passive friends. Go slow. Perhaps you can enlighten them. Help them redefine how passive should be perceived in the real world.

The current economic conditions handcuff the Fed and holds captive an upside move in rates which in turn, makes the bubble’s bubble a closer reality.

I’m no Lance Roberts however, I do believe stocks and bonds do vie for capital attention. Not based on an interest rate vs. equity earnings yield comparison, mind you. That’s just an ingenious Enron-like mathematical travail financial analysts devised to lead your portfolio into a high-risk, low-return trap and appear intelligent doing it. READ: Do Low Rates Justify Higher Valuations?

I am referring to the enduring nature of TINA, or “There Is No Alternative,” to stocks when the hefty lid on bond yields is considered. Warren Buffett on CNBC a few weeks ago called bonds “a lousy investment.” Why? Because who wants to extend their financial neck for a U.S. Treasury Note paying 2% plus for a decade?

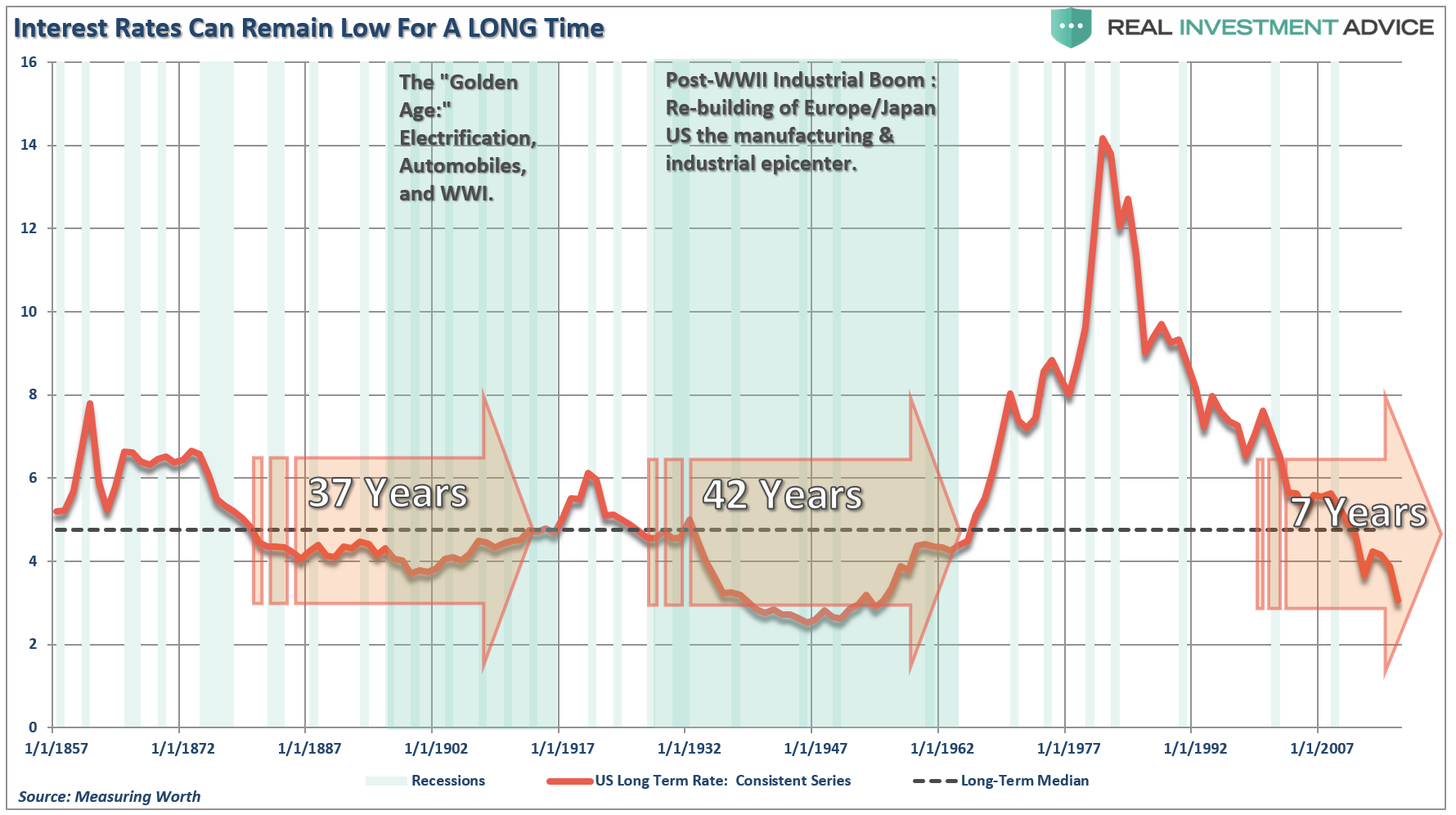

No doubt interest rates can remain low for extremely long spans. Several prolonged periods are mind boggling to comprehend as outlined in this chart from Lance Roberts.

Some wines are shorter to age.

From the 1981 peak to 2003, yields of prime corporate and long duration government bonds declined by a thousand basis points.

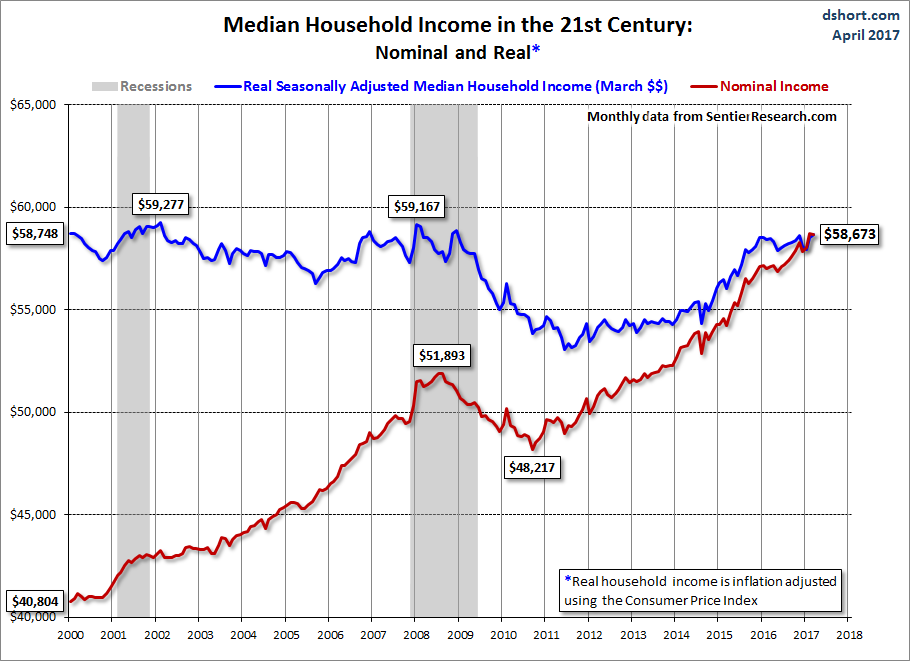

Intermediate and long-term interest rates are a function of economic growth and inflation. As economic activity heats up, so does the demand for credit. As wages increase, so does the ability of a household to meet or take on additional monthly debt obligations. Unfortunately, wage growth has been stubbornly stagnant for 17 years.

Sentier Research, a powerhouse of information which reflects the financial state of the American household, offers a monthly data for household incomes.

Adjusted for inflation which is most important, median household real income peaked at the beginning of the Great Recession. Sadly, inflation-adjusted income is still .7% below the beginning of the year 2000.

Inflation has been trending at roughly 2%; GDP growth which was disappointing for Q1 2017 is due for a big pick up in Q2 per the Atlanta’s Fed GDP Now’s forecasting model which is estimating as of May 16, a 4.1% annual rate. We’ll be monitoring at Real Investment Advice as this model is updated six or seven times a month with at least one update following seven economic data revisions from the BEA.

The Real Investment Advice estimate for GDP growth isn’t as optimistic as the Atlanta Fed’s. In addition, we have witnessed how the GDPNow forecast gets revised lower repeatedly as economic data is released.

In the United States, we have experienced a prolonged period of below-average economic growth since 2000 that may endure through 2022, when a positive demographic cycle emerges. Read: The Long View – Rates, GDP & Challenges.

Structural headwinds will keep longer duration yields subdued and the Fed handcuffed to raise short-term rates as quickly as they prefer. I’ve been a broken record with this commentary since I began to study Japan’s economy in 2009.

The book “The Holy Grail of Macroeconomics: Lessons from Japan’s Great Recession,” by economist Richard Koo, enlightened me to the similarities between the U.S. and Japan. The aftermath of deep recessions where household balance sheets are damaged combined with poor demographics, is a lethal structural blow to economic prosperity.

Overly accommodative central bank policies attempt to accelerate (they’re far from successful) or at the least, don’t stand in the way of recovery, which comes down to, for the U.S., a continued period of low interest rates.

The environment is perfect, as long as economic conditions just trudge along and the Fed is stuck, for the TINA monster to feed. Blame it on the demographics of an aging population, not enough young people forming households, excess debt, or poor savings rates. Pick your position. The backdrop is perfect for stocks to continue higher with sights near of the bubble’s bubble.

The continued positive momentum for stocks is a poor reason to let your guard down. On the contrary. More than ever as an investor, one must remain vigilant to take profits and rebalance. Stay humble. Understand the territory your wealth travels today can fall into a sink hole real fast.

Every long-term market cycle forges a unique path. Who knows how this one will crescendo. For now, I am sticking with the bubble’s bubble theory as I still observe too many Main Street investors who have some form of “spidey-sense” or talk doom when markets take in a short breath, which tells me after toiling in this industry since 1989, that the wall of worry that stocks climb, albeit aging like the nation’s infrastructure, is still intact.

However, when it crumbles, you can’t afford to get crushed.

I’m first and foremost a financial life planner, not a market analyst. However, when partnering with a client to create a retirement income distribution strategy, I fear now more than any other period since 2000, that sequence of return risk or a prolonged period of poor or zero portfolio returns, is a strong possibility in the future. After all, whether it’s through price or time, risk assets revert. It’s never different. As life goes, so do markets ebb and flow.

Oh, and the battle between the buy-and-holders and the risk managers?

It’ll be our financial civil war to fight; as an investor, whether choose to be or not, you will be pulled in unfortunately, by proxy. You see, your wealth will be on the line, the weapons chosen.

Yet again, we will fight.

You will bleed.

How much is up to you.

This article originally appeared on “Real Investment Advice”

Richard Rosso, MS, CFP, CIMA

Richard Rosso is the Head of Financial Planning for Clarity Financial. He is also a contributing editor to the “Real Investment Advice” website and published author of “Random Thoughts Of A Money Muse.” Follow Richard on Twitter.

Richard Rosso is the Head of Financial Planning for Clarity Financial. He is also a contributing editor to the “Real Investment Advice” website and published author of “Random Thoughts Of A Money Muse.” Follow Richard on Twitter.

I am with a financial group whom we have signed a fiduciary agreement. I am not sure as to what safety that this gives me , if any. So what do we do besides go to academia for the knowledge to do it ourselves? If i studied every thing that i will need to, there will not be any time for our other needs.This is all I would be doing. As the GUESS WHO would say ” I Got Got Got No Time! So what do we do?