Inflation continues to rise but may soon reach its peak. After that, its fate will be sealed: a gradual decline. Does the same await gold? If you like inviting people over, you’ve probably figured out that some guests just don’t want to leave, even when you’re showing subtle signs of fatigue. They don’t seem to care and keep telling you the same not-so-funny jokes. Even in the hall, they talk lively and tell stories for long minutes because they remembered something very important. Inflation is like that kind of guest – still sitting in your living room, even after you turned off the music and went to wash the dishes, yawning loudly.

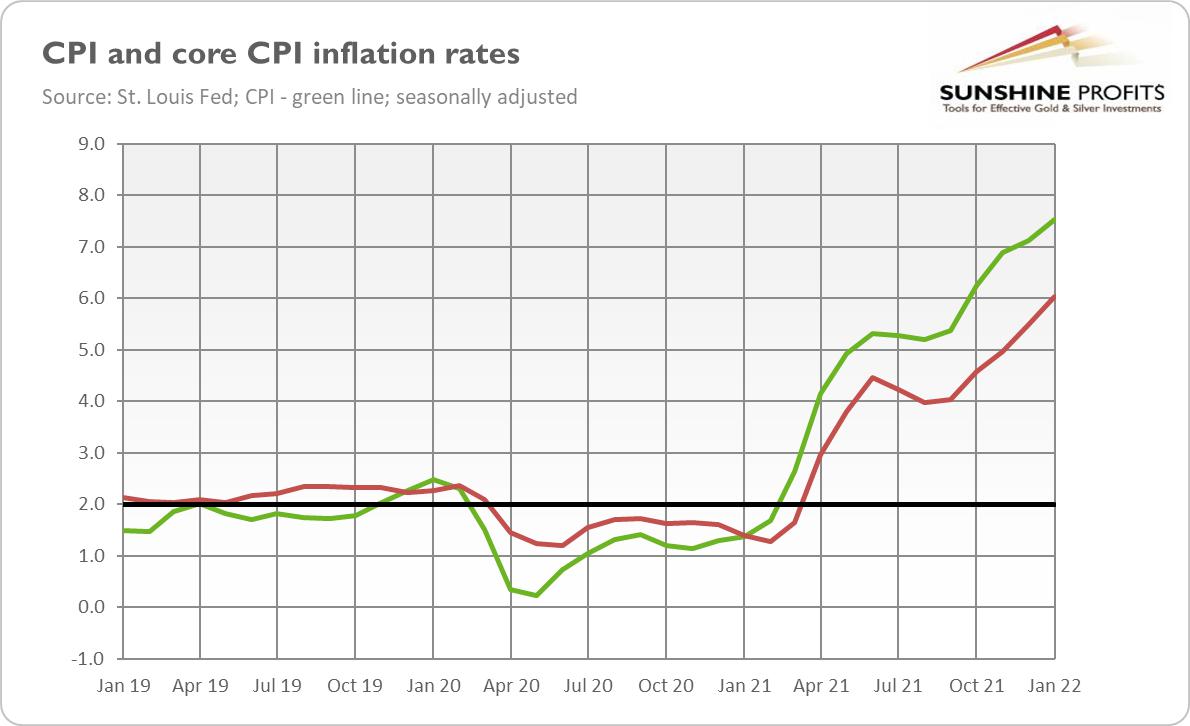

Indeed, high inflation simply does not want to leave. Actually, it’s gaining momentum. As the chart below shows, core inflation, which excludes food and energy, rose 6.0% over the past 12 months, speeding up from 5.5% in the previous month. Meanwhile, the overall CPI annual rate accelerated from 7.1% in December to 7.5% in January.

It’s been the largest 12-month increase since the period ending February 1982. However, at the time, Paul Volcker raised interest rates to double digits and inflation was easing. Today, inflation continues to rise, but the Fed is only starting its tightening cycle. The Fed’s strategy to deal with inflation is presented in the meme below.

What is important here is that the recent surge in inflation is broad-based, with virtually all index components showing increases over the past 12 months. The share of items with price rises of over 2% increased from less than 60% before the pandemic to just under 90% in January 2022.

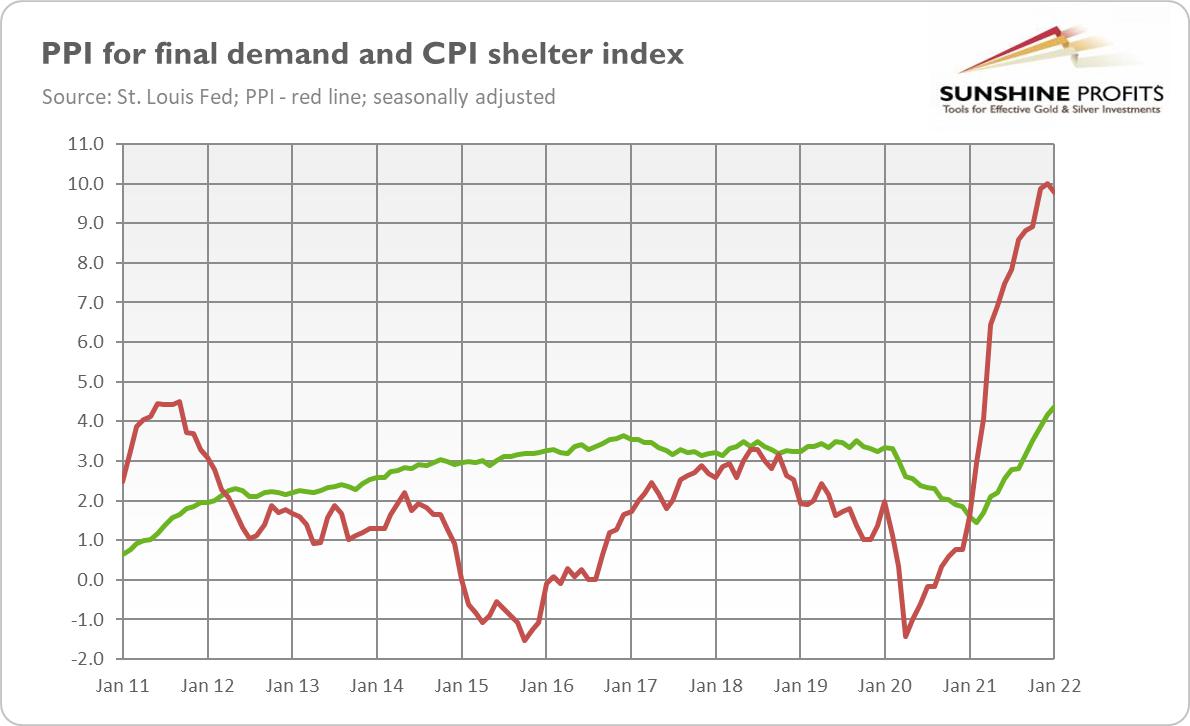

As the chart below shows, the index for shelter is constantly rising and – given the recent spike in “asking rents” – is likely to continue its upward move for some time, adding to the overall CPI. What’s more, the Producer Price Index is still red-hot, which suggests that more inflation is in the pipeline, as companies will likely pass on the increased costs to consumers.

So, will inflation peak anytime soon or will it become embedded? There are voices that – given the huge monetary expansion conducted in response to the epidemic – high inflation will be with us for the next two or three years, especially when inflationary expectations have risen noticeably. I totally agree that high inflation won’t go away this year.

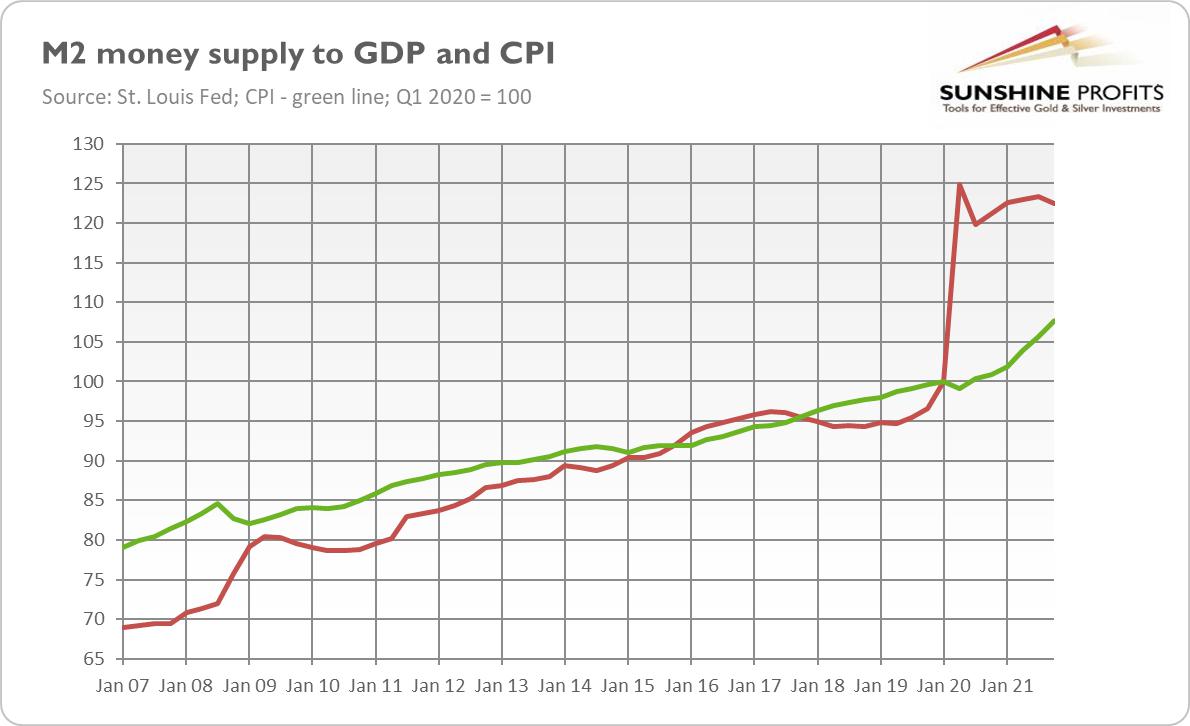

Please just take a look at the chart below, which shows that the pandemic brought huge jumps in the ratio of broad money to GDP. This ratio has increased by 23%, from Q1 2020 to Q4 2021, while the CPI has risen only 7.7% in the same period. It suggests that the CPI has room for a further increase.

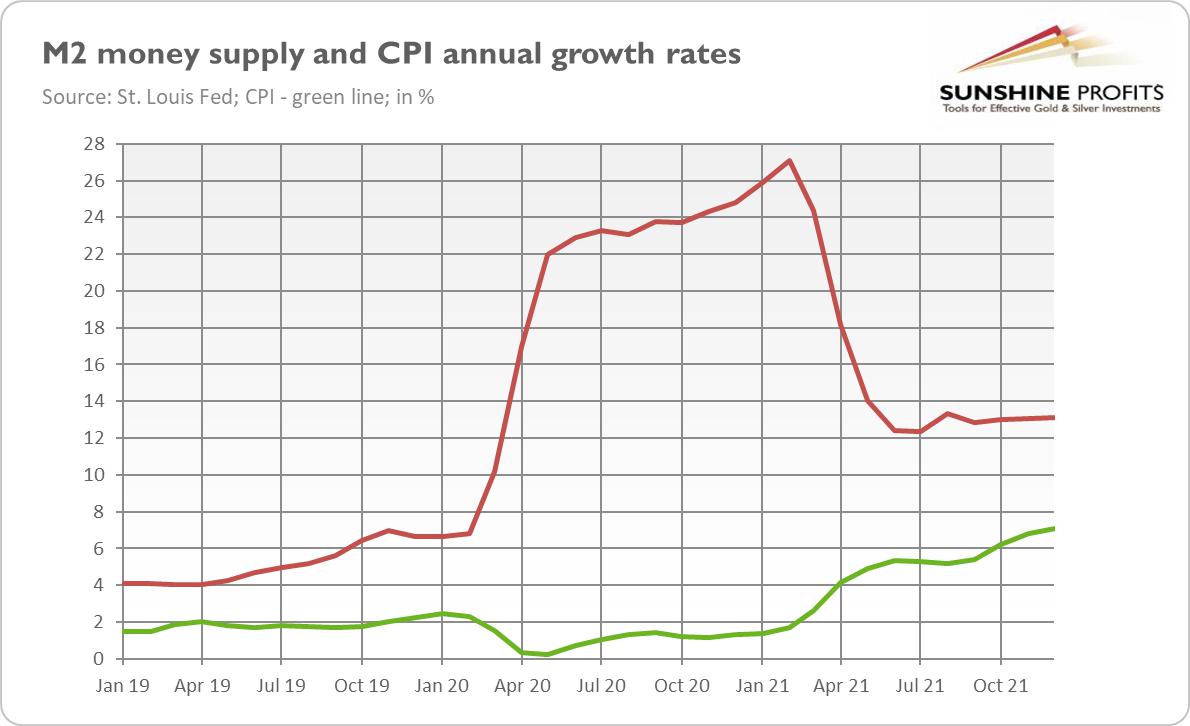

What’s more, the pace of growth in money supply is still far above the pre-pandemic level, as the chart below shows. To curb inflation, the Fed would have to more decisively turn off the tap with liquidity and hike the federal funds rate more aggressively.

However, as shown in the chart above, money supply growth peaked in February 2021. Thus, after a certain lag, the inflation rate should also reach a certain height. It usually takes about a year or a year and a half for any excess money to show up as inflation, so the peak could arrive within a few months, especially since some of the supply disruptions should start to ease in the near future.

What does this intrusive inflation imply for the precious metals market? Well, the elevated inflationary pressure should be supportive of gold prices. However, I’m afraid that when disinflation starts, the yellow metal could suffer. The decline in inflation rates implies weaker demand for gold as an inflation hedge and also higher real interest rates.

The key question is, of course, what exactly will be the path of inflation. Will it normalize quickly or gradually, or even stay at a high plateau after reaching a peak? I don’t expect a sharp disinflation, so gold may not enter a 1980-like bear market.

Another question of the hour is whether inflation will turn into stagflation. So far, the economy is growing, so there is no stagnation. However, growth is likely to slow down, and I wouldn’t be surprised by seeing some recessionary trends in 2023-2024. Inflation should still be elevated then, creating a perfect environment for the yellow metal. Hence, the inflationary genie is out of the bottle and it could be difficult to push it back, even if inflation peaks in the near future.

—

Editor’s Note: This article was first published by Sunshine Profits, and is reposted with permission.